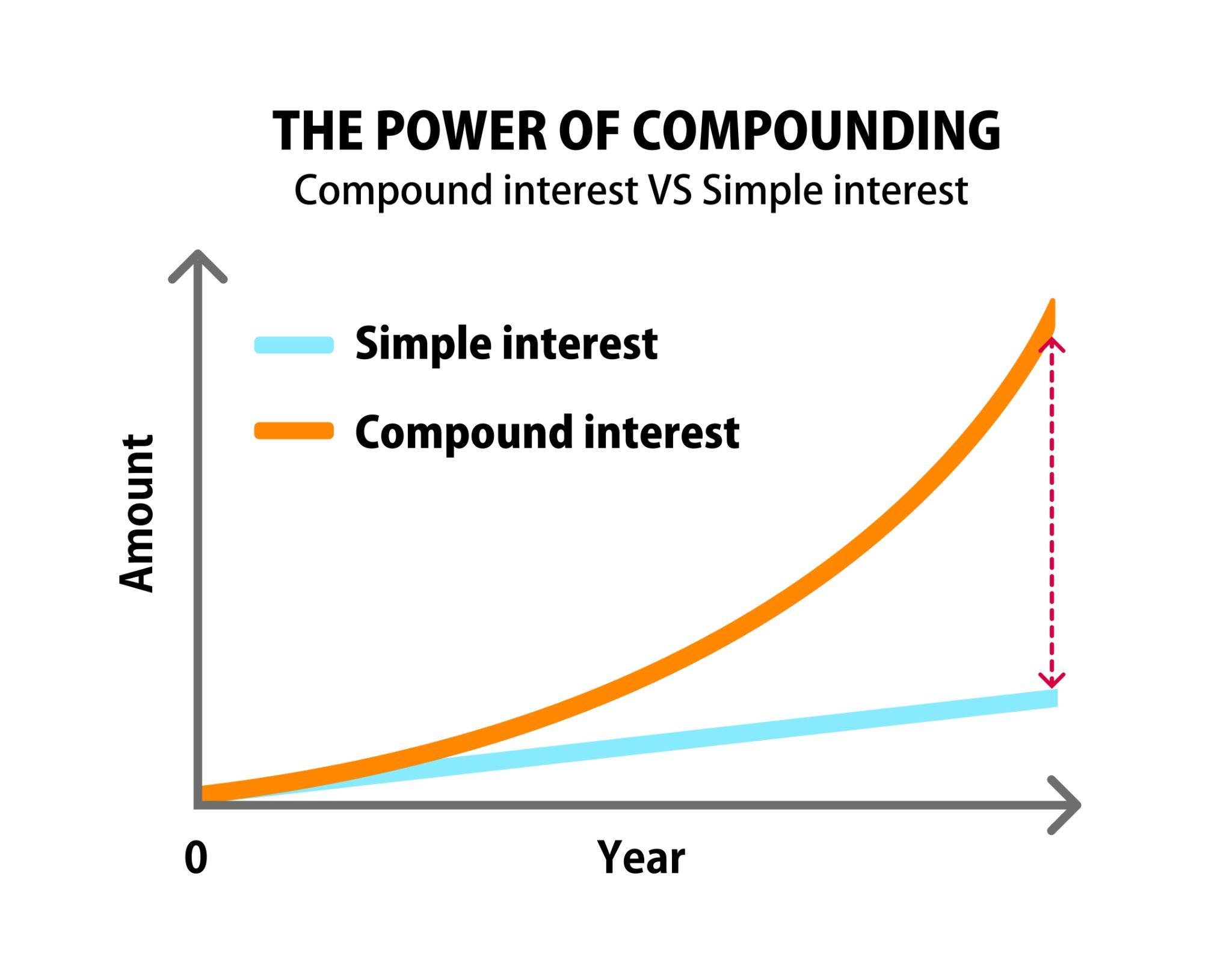

In the world of finance, few concepts hold as much transformative power as the compounding of interest. Often referred to by Albert Einstein as the “eighth wonder of the world,” compound interest is the process where the value of an investment grows exponentially because the earnings on an investment, both capital gains and interest, earn interest as time passes. While simple interest is calculated only on the principal amount of a loan or deposit, compound interest is calculated on the principal amount plus the accumulated interest from previous periods.

Understanding this mechanism is not merely an academic exercise; it is the cornerstone of successful long-term investing and personal financial management. Whether you are a novice saver or a seasoned investor, mastering the dynamics of compounding is essential to achieving financial independence.

Understanding the Mechanics of Compound Interest

At its most basic level, compounding is “interest on interest.” To appreciate its power, one must first understand how it differs from its linear counterpart and the specific variables that dictate its trajectory.

The Difference Between Simple and Compound Interest

Simple interest is calculated solely on the initial amount of money invested or borrowed, known as the principal. For example, if you invest $1,000 at a 5% simple interest rate for three years, you would earn $50 each year, totaling $150 in interest. Your total balance would be $1,150.

Compound interest, however, reinvests those earnings. In the same scenario with annual compounding, after the first year, you would have $1,050. In the second year, the 5% interest is calculated on the new balance of $1,050, resulting in $52.50 of interest. By the third year, the interest is calculated on $1,102.50. While the difference seems negligible in the short term, over decades, this “snowball effect” creates a massive divergence in total wealth.

The Variables: Principal, Rate, and Frequency

The velocity of compounding is determined by three primary factors:

- Principal: The initial sum of money. A larger starting point provides a broader base for interest to accrue.

- Interest Rate: The annual percentage rate (APR) or annual percentage yield (APY). Even a 1% difference in the interest rate can result in hundreds of thousands of dollars in difference over a 30-year investment horizon.

- Compounding Frequency: This refers to how often the interest is calculated and added back to the principal. Interest can be compounded annually, semi-annually, quarterly, monthly, or even daily. The more frequently interest is compounded, the higher the final return.

The Rule of 72: A Shortcut to Understanding Growth

To visualize compounding without a complex calculator, investors often use the “Rule of 72.” This is a simplified formula used to estimate the number of years required to double the invested money at a given annual rate of return. By dividing 72 by the annual rate of return, investors can get a rough estimate of how long it will take for their initial investment to grow. For instance, an investment with a 6% annual return will double in approximately 12 years (72 / 6 = 12). This rule highlights the exponential nature of growth: if you double your money every 12 years, a single $10,000 investment becomes $80,000 in 36 years.

The Role of Time in Exponential Growth

If interest rate is the engine of compounding, time is the fuel. The most critical element in the compounding equation is not the amount of money you start with, but how long you allow that money to grow undisturbed.

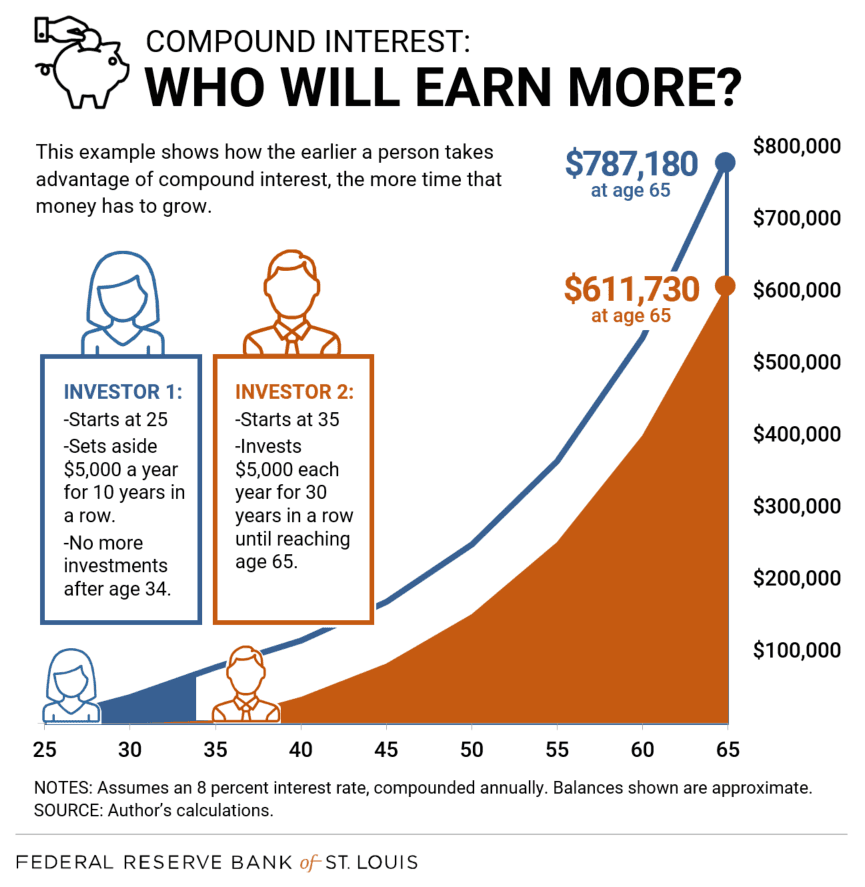

The Cost of Delay: Starting Early vs. Starting Late

The mathematical advantage of starting early is staggering. Consider two investors: Investor A starts investing $500 a month at age 25 and stops at age 35, never adding another cent. Investor B starts investing $500 a month at age 35 and continues until age 65.

Despite Investor B contributing significantly more total capital over 30 years, Investor A will likely end up with a larger portfolio at age 65 simply because their initial contributions had an extra decade to compound. This “head start” creates a gap that is almost impossible to bridge later in life, regardless of how much more money is contributed.

The Inflection Point: When Interest Outpaces Contributions

In the early stages of a savings plan, the growth of the account is driven primarily by contributions. If you save $1,000 a month, your balance grows mostly because you are putting money in. However, as the principal grows, the interest earned begins to do the heavy lifting.

The “inflection point” is the moment when the annual interest earned on the account exceeds the annual contributions made by the investor. Reaching this milestone is a psychological and financial turning point; it is the moment when your money begins working harder for you than you are working for your money.

Consistency Over Intensity

The power of compounding is often disrupted by the urge to “time the market” or by inconsistent savings habits. Compounding requires a “buy and hold” mentality. Every time an investor withdraws funds or stops contributing during a market downturn, they reset the compounding clock. Professional financial planning emphasizes staying the course, as the most significant gains in a compounding cycle occur in the final years of the investment period.

Strategic Applications in Personal Finance and Investing

Compounding is not just a theoretical concept; it is applied through specific financial vehicles designed to maximize long-term yields.

Harnessing Compound Interest in Retirement Accounts

Tax-advantaged accounts like the 401(k) or the Individual Retirement Account (IRA) are the ultimate tools for compounding. In a standard brokerage account, you may be taxed on dividends or capital gains annually, which acts as a “drag” on your compounding speed. In a 401(k) or IRA, your investments grow tax-deferred or tax-free (in the case of a Roth IRA). By eliminating the annual tax hit, 100% of your earnings remain in the account to compound year after year.

Reinvesting Dividends: Compounding Within the Stock Market

For equity investors, the Dividend Reinvestment Plan (DRIP) is a powerful way to leverage compounding. Instead of taking quarterly dividend payments as cash, a DRIP automatically uses those dividends to purchase more shares of the stock. This increases the total number of shares you own, which in turn increases the amount of the next dividend payment. Over time, the accumulation of shares through reinvested dividends can account for a substantial portion of a portfolio’s total return.

High-Yield Savings and Treasury Bonds

While the stock market offers higher potential returns, compounding also applies to lower-risk fixed-income assets. High-yield savings accounts and Certificates of Deposit (CDs) use monthly compounding to provide steady growth. Treasury bonds and corporate bonds also utilize compounding principles, particularly when interest payments (coupons) are reinvested into new bonds. For conservative investors, the certainty of compounding in these vehicles provides a reliable path toward wealth preservation and growth.

The Inverse Effect: When Compounding Works Against You

Compounding is a double-edged sword. While it can build immense wealth, it can also lead to financial ruin when applied to debt.

Credit Card Debt and High-Interest Loans

Credit cards are perhaps the most common example of “negative compounding.” Most credit card companies compound interest daily. If you carry a balance, you are not just paying interest on your purchases; you are paying interest on the interest from the previous day. With APRs often exceeding 20%, the debt can grow at a rate that far outpaces the borrower’s ability to pay it down, leading to a debt spiral.

The Erosion of Fees and Inflation

Two “silent killers” of compounding are investment fees and inflation. An investment management fee of 1.5% may seem small, but when compounded over 30 years, it can eat away nearly a third of your potential wealth. Similarly, inflation reduces the purchasing power of your money. If your investments are compounding at 5% but inflation is at 3%, your “real” rate of compounding is only 2%. To truly build wealth, an investor must seek returns that significantly outpace the rate of inflation after accounting for all fees.

Strategies to Mitigate Negative Compounding

The first step in any financial plan should be to eliminate high-interest debt. By paying off a credit card with a 24% interest rate, you are effectively “earning” a guaranteed 24% return on your money. Once debt is managed, focusing on low-cost index funds and tax-efficient strategies ensures that the maximum amount of capital remains in your control to compound positively.

Practical Steps to Maximize Your Compounding Potential

To make the most of compounding, one must move from understanding to action. The following strategies are utilized by successful investors to ensure their “wealth snowball” keeps rolling.

Automated Investing and Dollar-Cost Averaging

The greatest enemy of compounding is human emotion. By automating your investments, you ensure that contributions are made consistently regardless of market volatility. Dollar-cost averaging—investing a fixed amount of money at regular intervals—ensures that you buy more shares when prices are low and fewer when prices are high. This consistency is the bedrock upon which compounding thrives.

Optimizing Your Tax Strategy

Where you hold your assets matters as much as what you hold. By placing high-growth or high-dividend assets in tax-advantaged accounts and holding tax-efficient assets like index funds in taxable accounts, you minimize the “tax leakage” that slows down compounding. Professional financial advisors call this “asset location,” and it is a key component of a sophisticated investment strategy.

Maintaining a Long-Term Psychological Edge

Finally, the most successful compounders are those who possess patience. In a world of “get rich quick” schemes and daily market noise, the ability to wait 20 or 30 years for a strategy to bear fruit is a rare competitive advantage. Compounding is back-loaded; the results are often boring for the first decade and spectacular in the last. Developing the discipline to leave your investments alone is the final, and perhaps most difficult, step in mastering the art of compounding.

In summary, the compounding of interest is a fundamental force in the financial universe. It rewards the disciplined, the early, and the patient, while punishing those who fall into the trap of high-interest debt. By understanding its mechanics, respecting the power of time, and utilizing the right financial tools, anyone can harness this engine to build a secure financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.